As at 2020, disclosed institutional investment in African real estate had grown to $1.8bn, from $0.5bn in 2014. These investments were largely in the traditional real estate asset class including hospitality, office, and retail. Over the past few decades, these sectors, including high-end residential offered what investors required: dollarised rents from multinational tenants, a growing domestic middle and upper class, and financing structures modelled on the South African market.

On the other hand, alternative sectors like purpose-built student accommodation (PBSA), affordable housing and logistics have historically lacked the unit economics necessary to attract institutional capital at scale. The result was a structural concentration of capital in a few familiar sub-sectors, and not necessarily a reflection of where African real estate demand was largest, but where the market infrastructure was most legible to institutional underwriting.

As the market continues to mature, the unit economics for alternative property sectors are becoming more attractive. Data that we are tracking across student housing, healthcare and data centres shows a growing institutional appetite in these alternative assets and we believe that a number of them will drive Africa's real estate growth over the next decade. In this article, we will discuss five (5) of these alternative property sectors, profile existing operators in the market and why anyone active in the African property market should pay attention.

1. Purpose-Built Student Accommodation (PBSA)

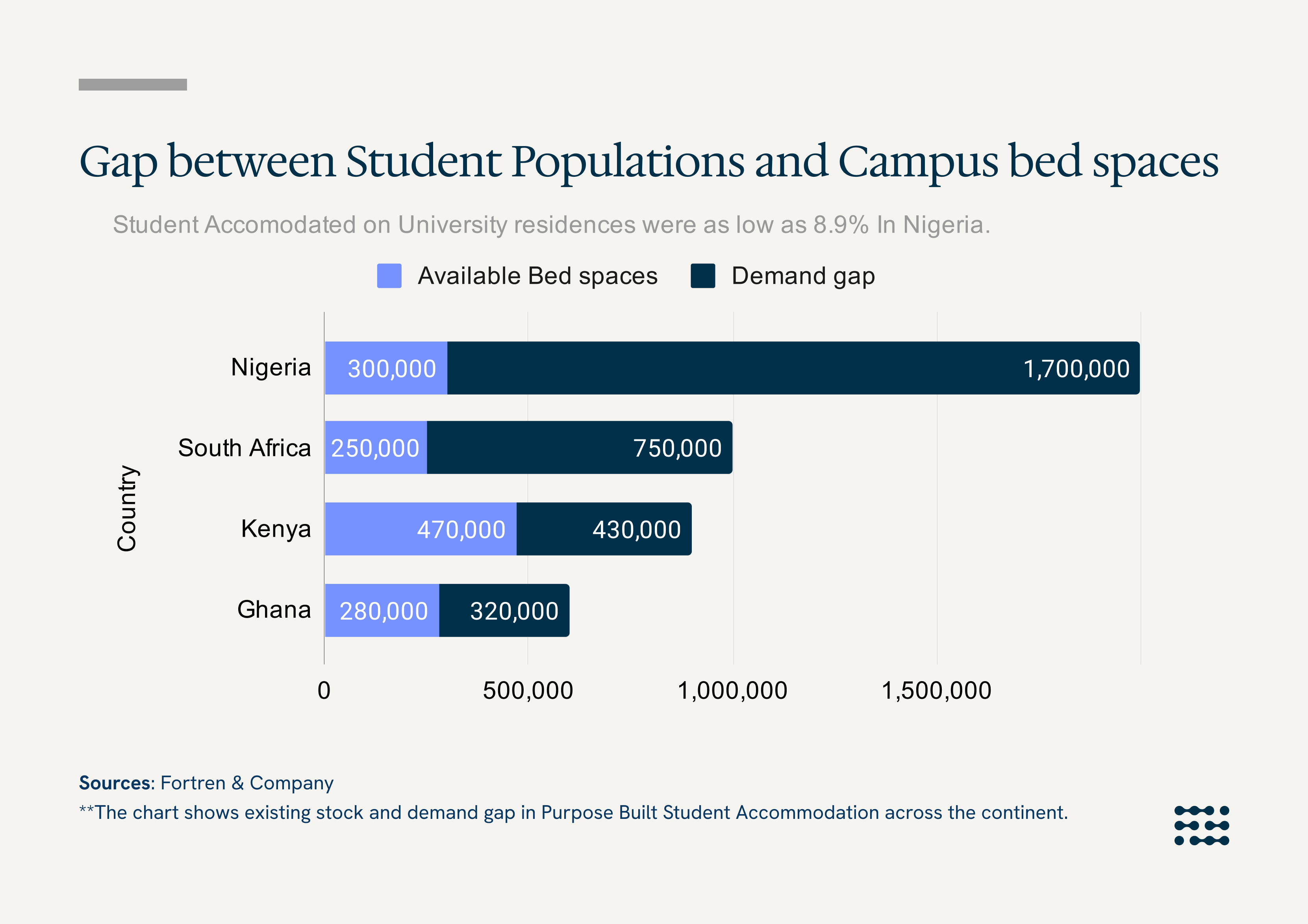

The investment case for African PBSA begins with a supply gap that is both quantified and widening. Student housing stock across the continent currently meets less than 30% of demand. Against that gap, Africa has 1,331 officially recognised higher education institutions with a gross enrolment ratio (GER) of 9%, compared to a global average of 42%. GER measures total enrolment in higher education as a percentage of the official age group population. With over 60% of Africa's 1.4 billion people under the age of 25, any upward movement in enrolment rates will translate into housing demand at a scale existing infrastructure cannot absorb.

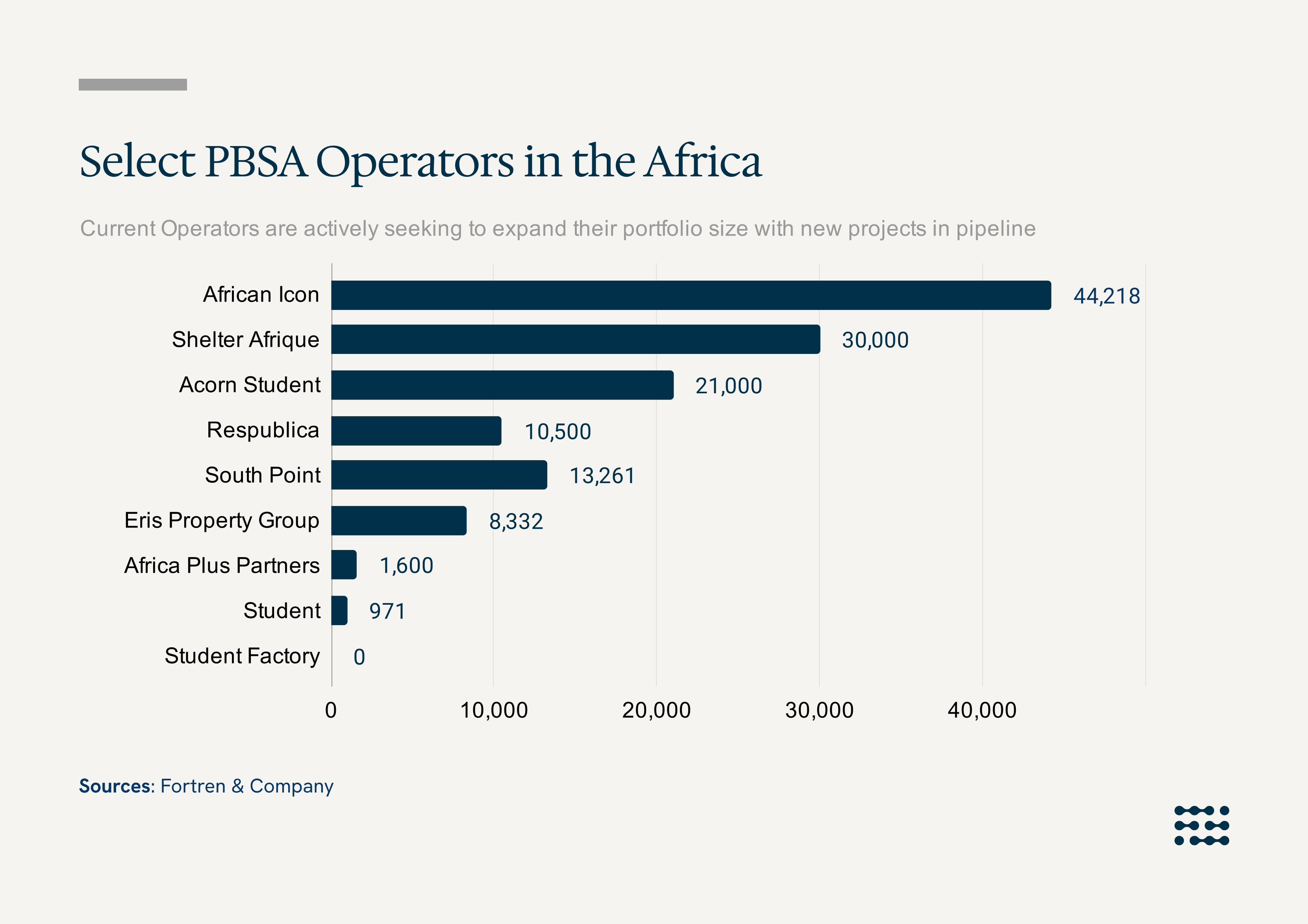

Operational data confirms the demand is real and recurring. Operators including Acorn Holdings, Eris, and Student Accommod8 have consistently reported strong occupancy. Acorn Holdings recorded 93% average occupancy in H1 2025, a figure that reflects a demand base that is demographically guaranteed rather than cyclically dependent. In mature markets like South Africa, PBSA delivers superior rental yield per square metre relative to conventional residential, with occupancy stability that most asset classes cannot match.

The principal constraint in price-sensitive markets like Nigeria has been affordability, the gap between what students can pay and what makes a project commercially viable. As student loan schemes and bursary programmes expand across the continent, that gap will narrow, and the investability of the sector will strengthen alongside it.

2. Industrial and Logistics Real Estate

The demand case for African logistics real estate is built on three reinforcing drivers: e-commerce growth, trade liberalisation, and a structural efficiency gap that is itself accelerating the need for modern infrastructure.

Africa's e-commerce market is projected to grow at a CAGR of 13.25%, reaching over $1 trillion by 2033. Urbanisation is concentrating consumer demand in dense metropolitan corridors, and an expanding middle class is shifting consumption from informal markets toward supermarkets, pharmacy chains, and organised retail, all of which require Grade A warehousing, cold storage, and integrated logistics networks to function at scale. The African Continental Free Trade Agreement (AfCFTA) compounds this, aiming to eliminate 90% of intra-African tariffs and catalyse integrated value chains along the Abidjan–Lagos, Cairo–Alexandria, Johannesburg–Pretoria, and Nairobi–Kampala corridors. The Economic Commission for Africa estimates intra-African trade will grow from 15% to 25% of total trade by 2040, unlocking an additional $20 billion in annual trade flows.

The efficiency gap reinforces the argument. In markets like Kenya, logistics costs account for approximately 30% of GDP, compared to 10–12% in developed economies. Every percentage point of improvement in logistics efficiency requires modern infrastructure, creating demand that is both large and durable. The launch of East Africa's first Industrial REIT, valued at $15 million on the Nairobi Securities Exchange in early 2026, marks the beginning of the sector's transition from fragmented and informal to professionally managed and investable. Concurrent port expansions at Dar es Salaam, Abidjan, Lomé, Maputo, and Mombasa, backed by World Bank funding, are de-risking the infrastructure context within which these assets will operate. For institutional investors, early positioning is what separates the returns.

3. Data Centres and Technology-Driven Spaces

Africa's data centre opportunity is a function of demand that already exists, a supply gap that is quantified, and regulation that is creating captive markets. Sub-Saharan Africa accounts for approximately three-quarters of global mobile money transaction volume and 65–66% of total transaction value out of a global total of $1.68 trillion. The region is projected to be the fastest-growing in mobile data traffic globally, at approximately 37% annually through 2028. Enterprise adoption of cloud services and SaaS is simultaneously shifting institutional IT workloads into co-location and hyperscale facilities. All of this requires physical infrastructure.

Africa's total data centre capacity currently sits at 360MW. McKinsey projects demand will grow from 0.4GW in 2025 to approximately 2.2GW by 2030, a fivefold increase requiring an estimated $10 billion to $20 billion in new investment, excluding fit-out costs. Against 126 operational facilities, 52 additional centres are in development or planning, pointing to a 32% capacity expansion by 2030, significant, but likely insufficient relative to demand.

.jpeg)

The regulatory dimension strengthens the case further. Over 74% of African countries have enacted data protection legislation enforcing data localisation requirements, structurally redirecting data hosting into regional markets and creating a policy-backed demand floor for in-country capacity. The U.S. International Development Finance Corporation and the IFC have committed $300 million and $250 million respectively to Africa Data Centres, while Equinix has announced a separate $390 million investment in South Africa. When capital of that scale and sophistication is already moving, the sector has passed the threshold from emerging opportunity to established asset class.

4. Healthcare Real Estate

Africa's healthcare real estate opportunity is underpinned by two converging demand pressures: a growing middle class able to pay for quality care, and a disease burden that is shifting the model of care delivery toward outpatient and specialist formats that require purpose-built real estate.

A growing middle class, rising per-capita incomes, and the rapid expansion of private health insurance are expanding the addressable market for private healthcare. Simultaneously, the rapid rise of non-communicable diseases — diabetes, hypertension, cancer, and cardiovascular illness is restructuring how care is consumed. Outpatient revenue has surged 45% since 2020, nearly triple the growth rate of inpatient services. The implication is direct: demand is shifting toward stand-alone dialysis centres, day-surgery clinics, diagnostic imaging centres, and medical plazas, all of which require compliant, purpose-built facilities that the existing stock cannot provide.

The senior care sub-sector adds a second layer. Countries including South Africa, Tunisia, Morocco, Egypt, and Mauritius are recording growing populations aged 65 and above. As urbanisation and migration erode traditional family care structures, purpose-built assisted living and skilled nursing facilities will move from a peripheral to a primary sub-sector within healthcare real estate.

5. Mid-Market Residential and Young Professional Housing

Africa's mid-market residential opportunity is a direct consequence of its demographic profile. The continent is home to approximately 1.5 billion people, projected to reach 1.9 billion by 2035, with almost 70% under the age of 30. This cohort is entering the workforce, forming new households, and generating sustained housing demand across every major urban market. 45.6% of Africa's population, approximately 720 million people, now live in cities. Within the next decade, Luanda and Dar es Salaam are projected to join Cairo, Kinshasa, Lagos, and Greater Johannesburg as megacities exceeding 10 million inhabitants, broadening the pipeline of urban housing demand well beyond a handful of gateway cities.

The product this cohort requires — co-living spaces, studio apartments, mini-flats, and furnished rentals, well-located relative to employment and transit, remains materially undersupplied across the continent. The demand base is large, structurally durable, and growing faster than supply can currently respond.

Final Thoughts

Each of the five sectors above is supported by the same underlying logic: a quantified demand gap, a structural driver that will not reverse, and a supply base that is materially insufficient relative to what is coming. The capital concentration in traditional real estate asset classes was a function of where market infrastructure was most developed, not where demand was most acute. As that infrastructure matures across alternative sectors, the allocation case becomes difficult to ignore.

For developers and investors, the strategic question is where to allocate, in what format, and through which structures.

We love your feedback. Let us know what you think about the African real estate market by sending an email to advisory@fortrenandcompany.com. You can also join the conversation here on LinkedIn.

If you need bespoke research on this market or any other asset class across the continent, send an email to our advisory team at advisory@fortrenandcompany.com

With just 3,577square meters in land mass, Lagos is home to over 17 million residents, making it one of the most densely populated cities in the world. One of the most pronounced effects of clear overpopulation in overcrowded cities like Lagos is the increase in informal settlements, land grabbing, and illegal construction. Internal data from the Lagos State government shows that more than 349 buildings have been erected illegally and do not comply with the planning laws set out by the state. In response, the Lagos State Building Control Agency (LASBCA) and the Ministry of Physical Planning and Urban Development have intensified enforcement of planning laws to ensure that buildings within Lagos State are designed, constructed, and maintained to a high standard of safety. Their enforcement efforts have led to numerous building demolitions and are primarily targeted at three recurring violations across the state, which we will be discussing below.

- Lack of building development permit:

- sdfds

-

Failure to obtain required development permits remains one of the most common triggers for demolition across Lagos. Under Section 27(1) of the Lagos State Urban and Regional Planning and Development Law, no building is allowed to be erected across the state, except when necessary permits and approvals have been duly sought and obtained. “No person shall carry out any development in Lagos State without obtaining a permit from the relevant planning authority.” Non-compliance with section 27(1) of the Lagos State Urban and Regional Planning and Development Law authorises the state government to demolish any building that has not sought and obtained the necessary approvals. Despite this clear guideline, unauthorised construction continues to proliferate in the state. In a recent enforcement action, 13 illegal buildingswere demolished in Lagos for non-compliance, highlighting the Government’s resolve to clamp down on developments that violate planning regulations. Several factors may explain why some developers bypass the approval process, including a lack of awareness of regulatory requirements, the perceived complexity or delay in obtaining permits, and, in some cases, a calculated risk to evade official fees or oversight. While these issues don’t justify non-compliance, they underscore the need for continued public education, transparency, and reform of the permitting process.

- Encroachment on Drainage Channels and Setbacks:

Building on drainage channels and designated setbacks stands out as one of the leading causes of demolition across Lagos. This issue not only breaches planning regulations but has also contributed to environmental and public safety risks.The Lagos State Building Control Agency(LASBCA) mandates a minimum setback of nine (9) meters for residential buildings in high-density, flood-prone zonessuch as Victoria Island, Apapa, and the Lekki Peninsula Schemes I and II. Despite these regulations, many developers have reclaimed and erected structures directly on waterways, obstructing water flow and increasing the risk of flooding. Recently, the Lagos state government marked 39 buildingsfor demolition in the Eti-Osa Local Government Area (mostly along the Ikota corridor) for obstructing drainage channels and encroaching.Similar actions have been taken in other areas like Amuwo Odofin. These demolitions have left many homeowners devastated. In response, affected owners have petitioned the government through their community associations, while others seek court injunctions to challenge the demolition or delay it pending clarification of their land status. Urban experts, however, emphasise the need for property buyers to secure proper planning permits from the Lagos StatePhysical Planning Permit Authority(LASPPPA) before embarking on any building or development project within the state.In many cases, properties built on canals, drainage channels, or government-designated right-of-way have little to no legal standing, making it difficult for affected owners to obtain compensation or favourable rulings in court. This is because such developments typically contravene established planning laws and are considered public safety hazards. We love your feedback. Let us know what you think about this article or your experience renting in Africa by sending an email toadvisory@fortrenandcompany.com. You can also join the conversation here onLinkedIn.

.jpg)

.jpeg)