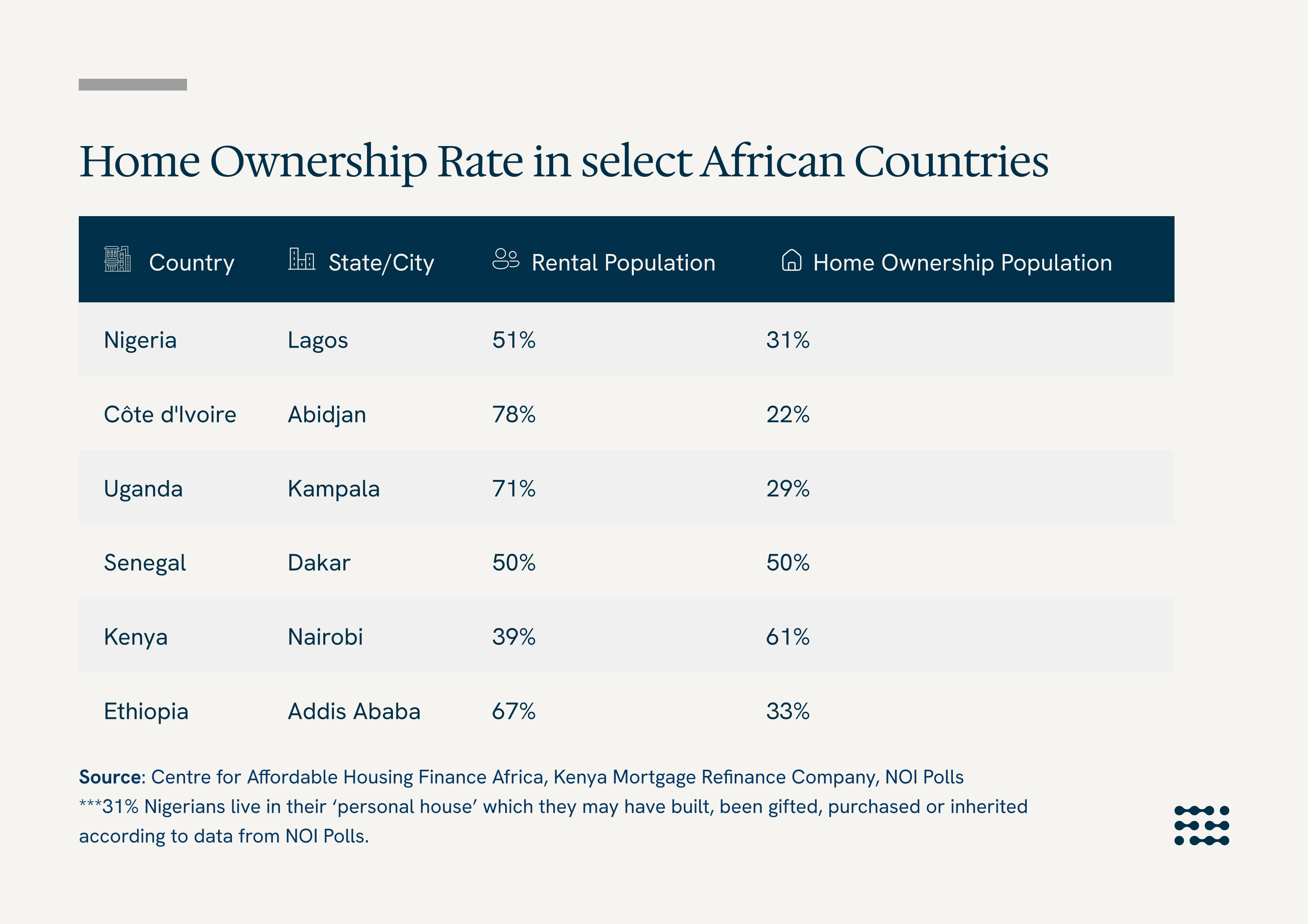

Africa's population has almost quadrippled over the past half century, from approximately 418 million in 1975 to an estimated 1.53 billion in 2025. Projections from the World Bank, the United Nations and the International Monetary Fund (IMF) suggest that the continent’s population will double by 2050 and Africa will be home to a quarter of the world’s population. With over 53 million units housing deficits, and less than 40% home ownership rate, these population projections if materialised will be the world’s biggest housing nightmares for two reasons. First, the continent’s housing deficit will at least double, exacerbating pressure in the rental market across the continent. Secondly, unlike the last century's mass emigration to the West, there is a growing trend with intra-continental migration and BLAXIT (reverse migration of black and African diaspora returning to the continent) adding further pressure to urban housing demand across the continent.

Beyond the well-documented housing gap, low ownership rates, and rising costs, Africa's rental market remains deeply opaque and poorly understood. Accurate, continent-wide data on what renting actually costs — across 54 countries (with significantly varying market dynamics) is scarce. For returning diaspora, expatriates, and mobile professionals deciding which African city to call home, that information gap makes objective comparison nearly impossible.

In this article, we will be comparing the true, all-in cost of renting across the continent providing a city-by-city breakdown of rental rate, how rents are actually being paid and the hidden costs across Africa’s most desired cities to help you compare and decide where to live.

The Cities Under the Lens

For the purposes of this article, we selected ten cities featured against three criteria: economic significance, expatriate and mobile professional activity, and rental market maturity. Together, these filters identify the cities where rental demand is highest, international tenants are most active, and the need for transparent benchmarking is most acute.

Each city is either a national economic capital or the dominant commercial hub within its sub-region. Each hosts a measurable expatriate and mobile professional population. And each has a sufficiently active private rental market to make meaningful, tier-by-tier comparison possible.

They also represent a geographically balanced selection spanning five sub-regions — West, Central, East, North, and Southern Africa. Our data covers ten cities and two neighbourhood tiers per city (high-end and mid-market).

.jpeg)

How does rental costs compare across Africa?

Abidjan is Africa's most expensive rental market in Africa, almost 2X more expensive than Cape Town. The city which has historically been the principal francophone gateway city in Africa, continues to serve as the primary commercial and cultural anchor for French-speaking populations across the continent and the broader diaspora. This structural demand concentration, compounded by a constrained high-quality supply base has established Abidjan as Africa's most premium residential rental market. Data we are tracking shows that 2 bedroom apartments in Abidjan’s high-end neighbourhoods are renting for $41,671 on average. A handful of luxury 2 bedroom penthouses are renting for as high as $127,766 or more.

Cape Town, Accra and Lagos followed as the second, third and fourth most expensive places to rent in Africa with 2 bedroom apartments in high-end neighbourhoods renting for $27,138, $26,299 and $19,379 respectively per annum.

Over the past few years, Cape Town has seen an influx of newcomers — South Africans escaping dysfunction elsewhere attracted by good jobs, and foreigners lured by its natural landscape and comparatively cheap values relative to other developed markets. Average rents have risen 68.5% since 2014, partly driven by a shortage of long-term rentals as landlords have migrated toward higher-returning short-term and tourist markets.Accra's premium is somewhat counterintuitive given its broader affordability profile, but it is explained by a highly concentrated high-end demand base particularly along the Cantonment, East Legon and Airport Residential Areas. Ghana's economy has experienced impressive growth over the past decade, making Accra one of West Africa's most important cities, attracting a dense cluster of multinationals, diplomatic missions, and NGOs, all competing for a very thin stock of high-end residential supply. Dollar-denominated expatriate housing allowances further inflate the top end of the market.In Lagos, high real estate prices are driven by limited land availability, high demand in prime areas, rising construction costs, speculation, and currency devaluation that has historically pushed developers to hedge by increasing prices. High-end residential stock in neighbourhoods like Ikoyi, Victoria Island, and Banana Island are typically dollar-denominated which compresses the high-end market into a very small geographic and socioeconomic band, sustaining elevated rents.It is important to note that when you compare on a project by project basis, the data becomes skewed. For instance, a number of ultra-luxury projects along the Bourdillion/Alexandra/Gerrard corridor in Ikoyi, Lagos are renting for as high as $130,000 annually.

The way rent is paid in Africa is making renting even more expensive

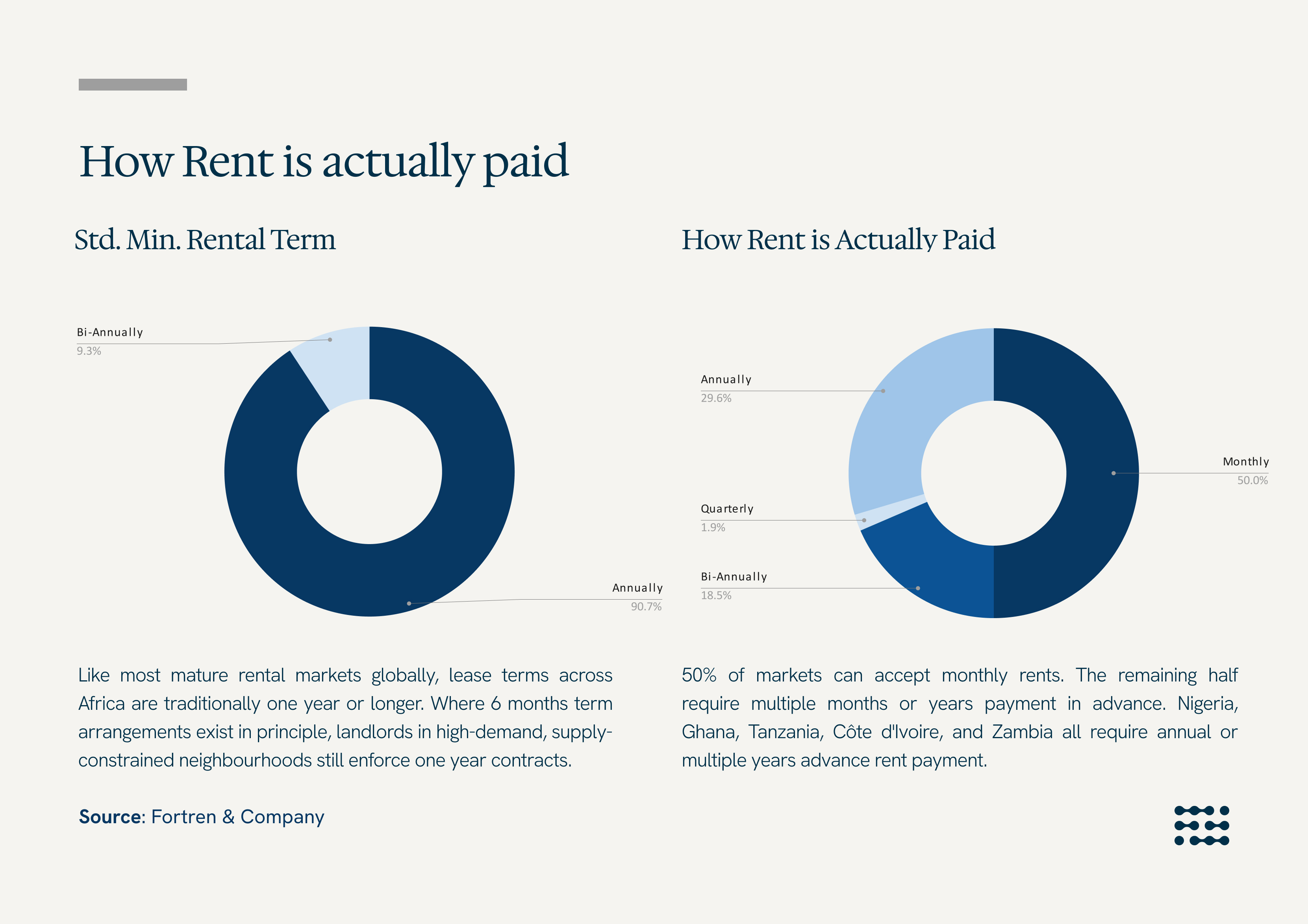

Africa’s rental market is one of the most rigid in the world. 50% of Africa’s traditional rental market requires at least 3 months of rent in advance. In countries like Nigeria, Ghana, Sierra Leone and Cameroon, demand far outstrips supply, giving landlords (who typically desire rapid capital recovery) leverage to charge 1 to 2 years rent in advance. In a generally low trust environment with limited access to credit data, landlords are more risk averse. For most landlords, the only path to building their capital base and protecting their rental income is by demanding several months/years rent in advance.

In nearly 91% of African cities, the typical lease term for traditional residential rental is one year. This is consistent with any market in the world where typical terms for rental contracts is one (1) year. When we dug deeper into how rents are actually being paid, we found that monthly rental payment is mostly adopted in the Southern African Development Community (SADC) countries, particularly in South Africa, Botswana and a handful of others. Although there is a growing advocacy for monthly rental structures across the continent, quarterly to yearly rent in advance is still the practice in a number of African countries, exacerbating the burden on renters.

While one-year contracts are standard for traditional empty space leases, it is important to note that furnished rentals are increasing allowing for shorter, monthly options. While monthly payments are sometimes possible in places like Eritrea, it is very common for landlords to request several months payment upfront, especially for newly occupied, furnished, or preferred units. Although recent government regulations have aimed to cap these upfront payments to ease the burden on tenants, it is still largely not enforced across the continent.

Despite the rigidity of advance payment requirements, the rent collection structure itself is surprisingly flexible, 42.3% of markets are fully flexible and 50% are moderately flexible, suggesting that while landlords demand large upfront sums, they may offer some accommodation in how those payments are structured or negotiated. A security deposit of one month’s rent is the standard norm, although landlords may sometimes request more depending on the property's risk or furnishing level.

The headline rent is rarely the full story.

The headline rent is rarely the full story. Across African cities, the true cost of securing a rental can exceed the first month's rent by a factor of three or more. Here is what to budget for.

Agency Fees: Paid by the tenant in most African markets, typically one to two months' rent or 10% of annual rent. Standard in Lagos, Accra, and Nairobi. Negotiable in softer markets, rarely so in high-demand areas.

Legal and Agreement Fees: A solicitor-drafted tenancy agreement is standard practice and attracts a fee of 5–10% of annual rent depending on the market. In Nigeria, this is borne by the tenant. It is not a cost worth skipping, an unvetted agreement is a significant liability.

Caution and Security Deposits: Typically one to three months' rent, held against damages or unpaid obligations. Refund practices are inconsistent. Lagos and Accra have a poor track record on returns. Document the property's condition at entry, in writing and photographically, without exception.

Stamp Duty and Government Levies: Some markets impose legally mandated stamp duty on tenancy agreements. Nigeria levies 0.78% of total rent value. Egypt and Morocco require notarisation fees. These are non-negotiable on a compliant lease.

Other Overlooked Costs: Utility connection deposits, internet installation, generator levies in markets with unreliable power, and service charges in managed buildings all compound the true annual move-in cost by a factor of three or more and in ways landlords rarely disclose upfront.

Conclusion

Renting in Africa is a financial commitment that demands far more planning than the headline rent suggests. For expats and returning diaspora, the stakes are high and this article is our attempt to provide you reliable data as you decide which African city to call home.

We love your feedback. Let us know what you think about this article or your experience renting in Africa by sending an email to advisory@fortrenandcompany.com. You can also join the conversation here on LinkedIn.

If you need bespoke research on any asset real estate class across the continent, send an email to our advisory team at advisory@fortrenandcompany.com

With just 3,577square meters in land mass, Lagos is home to over 17 million residents, making it one of the most densely populated cities in the world. One of the most pronounced effects of clear overpopulation in overcrowded cities like Lagos is the increase in informal settlements, land grabbing, and illegal construction. Internal data from the Lagos State government shows that more than 349 buildings have been erected illegally and do not comply with the planning laws set out by the state. In response, the Lagos State Building Control Agency (LASBCA) and the Ministry of Physical Planning and Urban Development have intensified enforcement of planning laws to ensure that buildings within Lagos State are designed, constructed, and maintained to a high standard of safety. Their enforcement efforts have led to numerous building demolitions and are primarily targeted at three recurring violations across the state, which we will be discussing below.

- Lack of building development permit:

- sdfds

-

Failure to obtain required development permits remains one of the most common triggers for demolition across Lagos. Under Section 27(1) of the Lagos State Urban and Regional Planning and Development Law, no building is allowed to be erected across the state, except when necessary permits and approvals have been duly sought and obtained. “No person shall carry out any development in Lagos State without obtaining a permit from the relevant planning authority.” Non-compliance with section 27(1) of the Lagos State Urban and Regional Planning and Development Law authorises the state government to demolish any building that has not sought and obtained the necessary approvals. Despite this clear guideline, unauthorised construction continues to proliferate in the state. In a recent enforcement action, 13 illegal buildingswere demolished in Lagos for non-compliance, highlighting the Government’s resolve to clamp down on developments that violate planning regulations. Several factors may explain why some developers bypass the approval process, including a lack of awareness of regulatory requirements, the perceived complexity or delay in obtaining permits, and, in some cases, a calculated risk to evade official fees or oversight. While these issues don’t justify non-compliance, they underscore the need for continued public education, transparency, and reform of the permitting process.

- Encroachment on Drainage Channels and Setbacks:

Building on drainage channels and designated setbacks stands out as one of the leading causes of demolition across Lagos. This issue not only breaches planning regulations but has also contributed to environmental and public safety risks.The Lagos State Building Control Agency(LASBCA) mandates a minimum setback of nine (9) meters for residential buildings in high-density, flood-prone zonessuch as Victoria Island, Apapa, and the Lekki Peninsula Schemes I and II. Despite these regulations, many developers have reclaimed and erected structures directly on waterways, obstructing water flow and increasing the risk of flooding. Recently, the Lagos state government marked 39 buildingsfor demolition in the Eti-Osa Local Government Area (mostly along the Ikota corridor) for obstructing drainage channels and encroaching.Similar actions have been taken in other areas like Amuwo Odofin. These demolitions have left many homeowners devastated. In response, affected owners have petitioned the government through their community associations, while others seek court injunctions to challenge the demolition or delay it pending clarification of their land status. Urban experts, however, emphasise the need for property buyers to secure proper planning permits from the Lagos StatePhysical Planning Permit Authority(LASPPPA) before embarking on any building or development project within the state.In many cases, properties built on canals, drainage channels, or government-designated right-of-way have little to no legal standing, making it difficult for affected owners to obtain compensation or favourable rulings in court. This is because such developments typically contravene established planning laws and are considered public safety hazards. We love your feedback. Let us know what you think about this article or your experience renting in Africa by sending an email toadvisory@fortrenandcompany.com. You can also join the conversation here onLinkedIn.

.jpeg)