Africa sits on one of the world's largest untapped student housing opportunities, but most investors are not looking.

Over the past 15 years, the total tertiary enrollment in Africa has doubled moving from 6 million in 2010 to over 12 million students in 2025 according to data from the British Council in Ethiopia. Although indicative of continental progress, this growth is creating significant strain on university housing systems. Across the continent, overcrowded dormitories, unsafe off-campus rentals, and informal living arrangements disrupt academic focus before studies even begin.

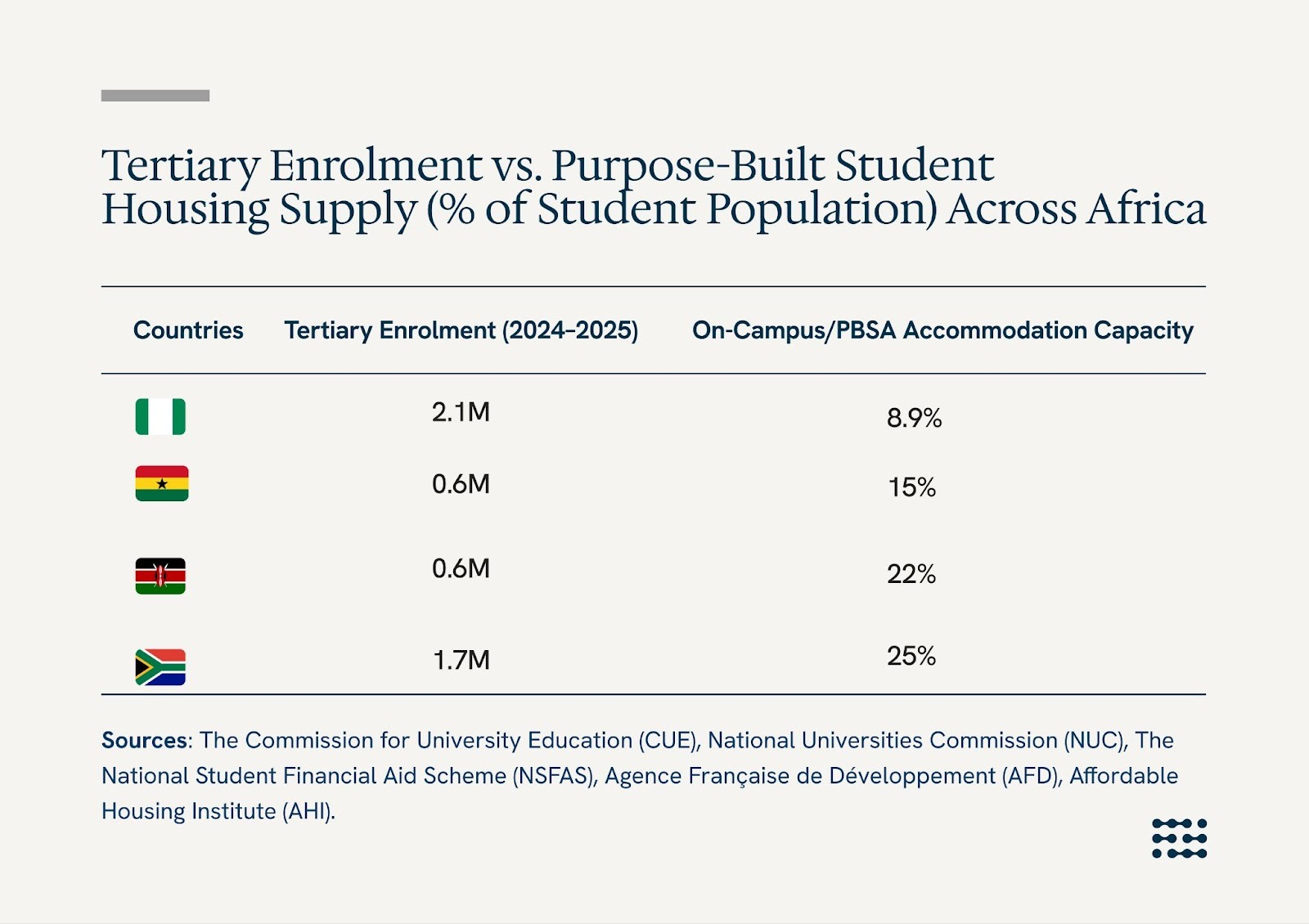

Over the past decade, the scale of the problem has become impossible to ignore. Africa’s tertiary enrolment has risen from 2.7 million students in 1991 to more than 12 million today, with UNESCO projecting that number could triple by 2040. Across many African public universities’ systems, on-campus housing supply remains limited. University accommodation rates vary widely across the continent with hostel to student ratio falling below 25% on average.

In Nigeria for instance, tertiary institutions are only able accommodate about 8.9% of their student population on average. In Kenya the average is about 22%, and major public universities in South Africa provide approximately one student bed for every 3.3 students, pushing the majority into a fragmented and often exploitative informal rental market within and outside campuses.

What makes this gap even more compelling is that it represents a measurable, largely untapped private sector investment opportunity. In the UK, Purpose-Built Student Accommodation attracted over £8.2 billion in private capital in 2022 alone. Africa, home to the world’s fastest-growing student population, captures only a fraction of that flow. The real question is not whether demand exists, but what it will take to unlock the private capital needed to meet it, and if it is viable enough to be worth their while. This article examines the scale of demand for student housing across Africa, the current level of private investment, and the structural barriers limiting capital flows into the sector. It also explores how student housing economics differ across African markets and outlines strategic solutions that could unlock large-scale private investment, but before we dive in, let’s look at the scale of the demand across different markets.

Nigerian tertiary institutions accommodates only 8.9% of its student population within Campus

Nigeria has the largest tertiary student population in Sub-Saharan Africa, with more than 2.1 million students enrolled in its universities, colleges and polytechnics. Less than 10% of these students can access campus hostels.

Even Mature South Africa can not accommodate up to 50% of its student population within Campus

As of 2025, South Africa’s higher education system had around 1.7 million students enrolled at universities and TVET colleges but only c.223,000 purpose-built student accommodation (PBSA) beds available leaving an estimated shortfall of over 500,000 beds.

Despite having one of the most private-sector driven student housing markets, Kenya accommodates only 22% of the student population on Campus

In Kenya, government-reported figures show public universities can house only about 22% of their students, leaving roughly 390,000 students without on-campus accommodation as of the 2023/24 academic year. This gap pushes students into high-demand private rentals near campuses.

Less than 20% of public university students in Ghana have access to formal on-campus accommodation

According to the Ghana Ministry of Education and the Ghana Statistical Service, tertiary enrolment in Ghana stood at 711,695 students in 2023. However, on-campus housing remains limited nationwide. For instance, the University of Ghana accommodates roughly 15% of its students, while Kwame Nkrumah University of Science and Technology has about 85,000+ students enrolled with less than 20,000 available beds. Overall, less than 20% of public university students in Ghana have access to formal on-campus accommodation, leaving the majority reliant on private hostels in Accra and Kumasi.

Despite the glaring supply-demand imbalance, there is clearly not enough private investment in the African Purpose-Built Student Accommodation (PBSA) market.

South Africa accounts for c.90% of formal Purpose-Built Student Accommodation (PBSA) supply on the continent, supported by a mature REIT framework, institutional participation and dedicated players like Respublica, Eris Property Group and South Point. Outside of South Africa, the landscape is dominated by small-scale, "mom-and-pop" developers who provide informal or semi-formal housing that lacks the security, amenities, and scale required by institutional capital.

There are, however, emerging institutional signals in other parts of the continent. In Kenya for instance, Acorn Holdings has successfully pioneered the KES 5.7 billion green bond market issued in 2019, the first Green Bond in Africa to be listed on both the Nairobi Securities Exchange and the London Stock Exchange. The student housing focused fund has also financed the development of over 7,000 student beds across eight purpose-built student accommodation properties in Kenya, including Qwetu and Qejani developments.

Similarly, in Nigeria, student housing has not been institutionalised or seen enough private sector interest. A number of boutique development firms like Student Accommod8 are attempting to institutionalize the sector by providing purpose built student accommodation (PBSA) with 15,000 beds in the next 5 years to Nigerian and West African tertiary institutions.

When compared to the £50 billion+ global PBSA investment volumes seen annually in Europe and North America, Africa’s share remains statistically marginal. The capital is ready, but it is currently stuck behind a wall of perceived and structural risks.

The Barriers to Entry: Why Capital Remains Cautious

If the demand is "recession-proof" and the demographic tailwinds are so strong, why isn't more private capital flowing in? The answer lies in a complex matrix of macroeconomic and operational hurdles.

1. Return & Paying Power Mismatch

Private capital is not biased, and typically favours the highest bidder (investments that deliver the best financial returns). When compared to alternative investments, student housing is generally less financially attractive to private investors. This is because students are price sensitive, due to their limited disposal income. This is the central paradox of African PBSA. There is a ceiling on how much a student can pay, and in most cases, is not sufficient to be worth a private investor's while, especially when there’s an array of higher yielding alternatives.. This mismatch extends beyond returns and purchasing power; it also reflects a fundamental gap in quality expectations. Investors typically prefer to build or invest in premium–standard facilities to justify institutional capital deployment. However, the vast majority of the estimated 12 million students are price sensitive and can not pay for premium. Bridging this affordability gap, while maintaining the service standards expected by institutional and impact investors remains one of the most significant operational challenges in the student housing market.

2. Currency Volatility and Repatriation Risk

For foreign institutional investors, the primary deterrent is FX risk. While a student housing project in Lagos or Nairobi may generate impressive yields in local currency, those gains can be wiped out instantly by currency devaluation. Since most large-scale funding is sourced in USD or EUR, the mismatch between dollar-denominated debt and local-currency revenue makes long-term modeling nearly impossible for conservative funds.

3. High Cost of Capital and Construction

In many African markets, commercial lending rates typically range between 18% and 35%, significantly increasing the cost of capital for real estate development. At such borrowing costs, projects can only remain viable if exit cap rates compress substantially, a condition that is often difficult to achieve in still-maturing property markets. At the same time, construction costs are elevated by heavy reliance on imported finishing materials and the limited availability of specialised student-housing contractors. Together, these factors push the cost per bed well above the affordability threshold for the average student, creating a structural challenge for developers seeking to deliver financially viable student housing at scale.

4. Land Tenure and Regulatory Complexity

Sourcing and securing properly titled land near major universities remains a significant structural hurdle. Land ownership disputes, opaque titling processes, and lengthy permitting cycles frequently extend project timelines by several years. In addition, many African universities sit on state-owned land, requiring developers to structure projects through complex Public-Private Partnership (PPP) arrangements. However, in many markets, the institutional capacity required to structure, negotiate, and enforce these frameworks remains limited, introducing additional uncertainty for private capital seeking to enter the sector.

The Economics of African Student Housing: A Different Math

The economics of a student housing bed in Africa differ significantly from those in the Global North. In markets like the UK or the US, what may appear ‘luxury’ from an African perspective is often simply the baseline standard of student accommodation there; functional, regulated, and built to expected living standards. In contrast, many African markets are still addressing gaps in basic quality, supply, and infrastructure, which fundamentally shapes the pricing and positioning of PBSA.

- Yield Compression: In mature markets, investors accept yields of 3.5–4.5%. In Africa, due to the high-risk premium, investors target 12-18% unlevered yields.

- Operational Intensity: Unlike traditional residential rentals, student housing is operationally heavy. It requires managing high turnover, intensive maintenance, and providing ancillary services like high-speed internet and laundry. In most African markets, this also includes providing redundant infrastructure like solar power, water boreholes, and private security, which adds to the operating expense (OPEX).

- The Parental Guarantee & Student Credit Gap: In the West, student housing is secured by parental guarantees or sophisticated credit scoring. In many African markets, where the informal economy is dominant, verifying the creditworthiness of a guarantor is difficult, leading to higher default risks or the need for innovative pay-as-you-go digital collection models.

Strategic Solutions: Unlocking the Floodgates

To move from informal rentals to an institutional asset class, a collaborative approach is required between the state, universities, and the private sector.

1. Innovative Financing (Green Bonds and REITs)

We must move away from short-term bank debt. The success of Acorn's Green Bond in Kenya proves that there is an appetite for debt instruments that align with ESG (Environmental, Social, and Governance) goals. Governments should also provide tax incentives for Student Housing REITs, allowing retail and institutional investors to pool capital and gain liquidity.

2. Credit Enhancement and Blended Finance

International Development Finance Institutions (DFIs) like the IFC (International Finance Corporation) or AfDB (African Development Bank) can play a pivotal role by providing first-loss guarantees or FX hedging instruments. By de-risking the currency volatility, they can make African PBSA projects palatable for international pension funds.

3. Standardization of PPP Frameworks

Universities should stop trying to be landlords and instead act as land partners. By providing long-term land leases (50+ years) to private developers in exchange for a share of revenue or a fixed number of affordable beds, universities can solve their housing crises without taking on debt.

4. Alternative Building Technologies (ABT)

To solve the affordability crisis, developers must embrace modular construction and 3D printing. Reducing construction time by 30% and material waste by 20% can significantly lower the rent-per-bed required to achieve a target IRR.

Final Thoughts

The African student housing market is no longer a niche of interest; it is becoming a core pillar of the continent's economic infrastructure. With Africa’s expanding youth population and rising tertiary enrolment, demand is accelerating far faster than the supply of quality accommodation. Existing infrastructure is already under strain and without significant private investment, the gap will continue to widen.

Although challenges such as high financing costs, currency volatility, and regulatory complexity persist, these are characteristic of markets in the early stages of institutionalization rather than structural weaknesses.As the sector formalizes, African student housing is transitioning into a scalable, income-generating asset class with defensive fundamentals and long-term growth visibility and investors should pay attention.

We love your feedback. Let us know what you think about Africa’s Student Housing Market by sending an email to advisory@fortrenandcompany.com. You can also join the conversation here on Linkedin.

If you need a bespoke research on this market or any other asset class across the continent, send an email to our advisory team at advisory@fortrenandcompany.com.

With just 3,577square meters in land mass, Lagos is home to over 17 million residents, making it one of the most densely populated cities in the world. One of the most pronounced effects of clear overpopulation in overcrowded cities like Lagos is the increase in informal settlements, land grabbing, and illegal construction. Internal data from the Lagos State government shows that more than 349 buildings have been erected illegally and do not comply with the planning laws set out by the state. In response, the Lagos State Building Control Agency (LASBCA) and the Ministry of Physical Planning and Urban Development have intensified enforcement of planning laws to ensure that buildings within Lagos State are designed, constructed, and maintained to a high standard of safety. Their enforcement efforts have led to numerous building demolitions and are primarily targeted at three recurring violations across the state, which we will be discussing below.

- Lack of building development permit:

- sdfds

-

Failure to obtain required development permits remains one of the most common triggers for demolition across Lagos. Under Section 27(1) of the Lagos State Urban and Regional Planning and Development Law, no building is allowed to be erected across the state, except when necessary permits and approvals have been duly sought and obtained. “No person shall carry out any development in Lagos State without obtaining a permit from the relevant planning authority.” Non-compliance with section 27(1) of the Lagos State Urban and Regional Planning and Development Law authorises the state government to demolish any building that has not sought and obtained the necessary approvals. Despite this clear guideline, unauthorised construction continues to proliferate in the state. In a recent enforcement action, 13 illegal buildingswere demolished in Lagos for non-compliance, highlighting the Government’s resolve to clamp down on developments that violate planning regulations. Several factors may explain why some developers bypass the approval process, including a lack of awareness of regulatory requirements, the perceived complexity or delay in obtaining permits, and, in some cases, a calculated risk to evade official fees or oversight. While these issues don’t justify non-compliance, they underscore the need for continued public education, transparency, and reform of the permitting process.

- Encroachment on Drainage Channels and Setbacks:

Building on drainage channels and designated setbacks stands out as one of the leading causes of demolition across Lagos. This issue not only breaches planning regulations but has also contributed to environmental and public safety risks.The Lagos State Building Control Agency(LASBCA) mandates a minimum setback of nine (9) meters for residential buildings in high-density, flood-prone zonessuch as Victoria Island, Apapa, and the Lekki Peninsula Schemes I and II. Despite these regulations, many developers have reclaimed and erected structures directly on waterways, obstructing water flow and increasing the risk of flooding. Recently, the Lagos state government marked 39 buildingsfor demolition in the Eti-Osa Local Government Area (mostly along the Ikota corridor) for obstructing drainage channels and encroaching.Similar actions have been taken in other areas like Amuwo Odofin. These demolitions have left many homeowners devastated. In response, affected owners have petitioned the government through their community associations, while others seek court injunctions to challenge the demolition or delay it pending clarification of their land status. Urban experts, however, emphasise the need for property buyers to secure proper planning permits from the Lagos StatePhysical Planning Permit Authority(LASPPPA) before embarking on any building or development project within the state.In many cases, properties built on canals, drainage channels, or government-designated right-of-way have little to no legal standing, making it difficult for affected owners to obtain compensation or favourable rulings in court. This is because such developments typically contravene established planning laws and are considered public safety hazards. We love your feedback. Let us know what you think about this article or your experience renting in Africa by sending an email toadvisory@fortrenandcompany.com. You can also join the conversation here onLinkedIn.

.jpg)

.jpeg)